Ako nakupovať

Ako nakupovaťDoručenie

Nákupný poradca

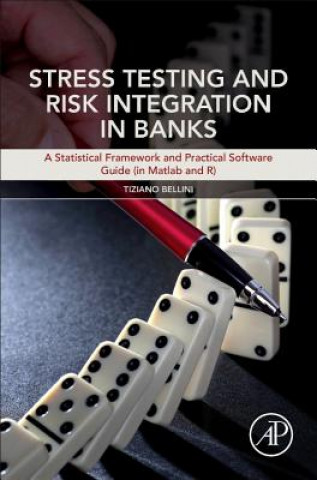

Stress Testing and Risk Integration in Banks

Angličtina

Angličtina

309 b

309 b

30 dní na vrátenie tovaru

Mohlo by vás tiež zaujímať

/

Pevná

/

Pevná

44.07

€

44.07

€

/

Brožovaná

12.87

€

/

Brožovaná

12.87

€

Stress Testing and Risk Integration in Banks: A Statistical Framework and Practical Software Guide (in Matlab and R) provides a comprehensive view of risk management that emphasizes the stress testing process. Using a bottom-up risk integration strategy, the book presents a multi-country bank prototype to assess bank solvency in periods both long (economic capital) and short (liquidity mismatching). Following the perspective of commercial banks, it concentrates on information available in the risk management practice to propose an easy-to-implement statistical framework that is the natural basis for stress testing analysis. To help readers, users will find a formal statistical setting enriched with examples, business cases, and exercises worked in Matlab and R that facilitate an easy application of the methodology in daily risk management practices. Provides a rigorous statistical framework for risk assessment Follows an integrated bottom-up approach to risk modeling central to U.S. Federal Reserve FRB CCAR (Comprehensive Capital Analysis Review) and U.K. PRA (Prudential Regulatory Authority) approaches, as well as Basel III (and Solvency IIProvides numerous sample codes

Informácie o knihe

Angličtina